Checked your bank account lately? That interest rate is not pretty. Banks are cutting rates across Singapore. Your hard-earned savings are earning less each day. It feels like running on a treadmill. You save and save, but get nowhere. So, what can you do about it? Many Singaporeans on HardwareZone are asking the same question. They are finding new ways to make their money work harder. Here is what they are talking about.

The Rate Cut Reality

The golden age of high interest seems to be over. Singaporeans are noticing big changes. Banks are adjusting their strategies. This directly impacts your savings. It is more important than ever to stay informed and adapt.

- Traditional savings are losing steam

Fixed Deposit rates are dropping fast. Major banks like BOC and ICBC have already cut their rates. Singapore Savings Bonds (SSB) are not much better. The projected 10-year average return is now very low. This makes safe havens less attractive for growing cash.

“The FDs rates now all lower than all the normal deposit promo, no point locking in anymore.”

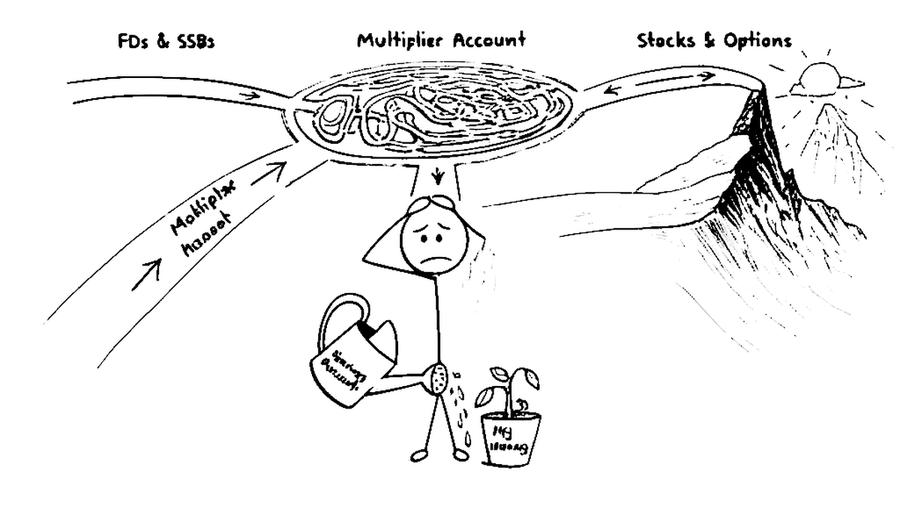

- High-yield accounts have more hoops

Accounts like the DBS Multiplier are a popular choice. But banks are making them more complex. They offer attractive promos, like higher caps for Treasures clients. However, these deals are often temporary and exclusive. This leaves many everyday savers feeling left out.

“Aiya, for 3 months only”

- Banks want more than your deposits

To get the best rates, you need to do more. Banks now reward you for using their other services. This includes investments, insurance, and credit card spending. They want to be your all-in-one financial hub. Simply parking your money is no longer enough to earn high interest.

“in simple words, they want more than just parking $ with them, they want you to spend via them”

The Kiasu Investor’s Dilemma

With safe options yielding less, what is next? Many Singaporeans face a tough choice. Sticking with low rates feels safe but unproductive. Exploring new options feels risky. This creates a few key challenges for the everyday investor trying to get ahead.

- Fear of complexity and risk

The leap from FDs to stocks or options is huge. Many are wary of markets they do not understand. The perceived risk of losing capital is a major barrier. This keeps people in low-yield accounts, even when they are unhappy with the returns.

“We are not familiar with US market let alone Options, which is an art by itself.”

- Information overload and confusion

Bank promotions come with complicated terms. It is hard to know which rules apply. Can you combine offers? What counts towards your balance? This confusion can be frustrating. It makes optimizing your savings feel like a full-time job.

“This Promotion is not to be used in conjunction with any other ongoing Deposits promotion offers.”

- Age and life stage limitations

Financial strategies are not one-size-fits-all. A young person can afford to take more risks. Someone nearing retirement cannot. Older Singaporeans often find fewer suitable products. They need safe, reliable income, but options are shrinking.

“Should at least come up with a simple plan for 60yo and above to continue the game”

Your Money, Your Move

Feeling stuck is normal. But you have options. HardwareZone users are sharing practical steps. You can take control of your finances. It starts with small, smart actions. Here are three strategies people are using right now.

- Maximise your existing accounts

Do not just let your money sit. Understand the rules of your high-yield account. For DBS Multiplier, find low-cost ways to hit more categories. A small monthly investment or insurance premium can unlock higher interest on your entire savings balance.

“30k account value on lowest tier on transaction amount, can earn about $80 more per year if I do $100 RSP on MBH”

- Build safer, alternative income streams

Even with lower rates, consistency helps. Some users stagger their T-bill or SSB maturities. This ensures they have a steady flow of cash coming in. It is a disciplined, low-risk way to create predictable income without touching complicated investments.

“I staggered T-bill subscriptions over the past few years so that they mature over several months rather than all at once.”

- Learn about calculated risks

If your risk appetite allows, start learning. You do not have to jump straight into complex trades. Many begin with safer investments like S&P 500 ETFs. Education is key. The goal is to make informed decisions, not gamble your savings away.

“I put my foot in the US stock market by just buying S&P 500 few years ago and saw very good growth back then”

The financial landscape in Singapore is changing. Low interest rates are the new normal. Sitting back is no longer a viable strategy. It is time to be proactive. Whether you are squeezing more out of your savings account or learning about ETFs, every small step counts. Take charge of your money today.

Read the original discussions on HardwareZone: